5 Things Every First-Time Homebuyer Should Know About Mortgages

Scouring the property market to find a property you want to buy is the fun part – but then comes the serious business of securing a mortgage. First-time buyers have a lot to learn on their journey and it’s easy to be confused by all information and lingo being used by lenders, real estate agents and other industry experts.

To make things easier to understand, we’ve put together 5 things every first-time homebuyer should know about mortgages, which we hope will help you make more informed decisions.

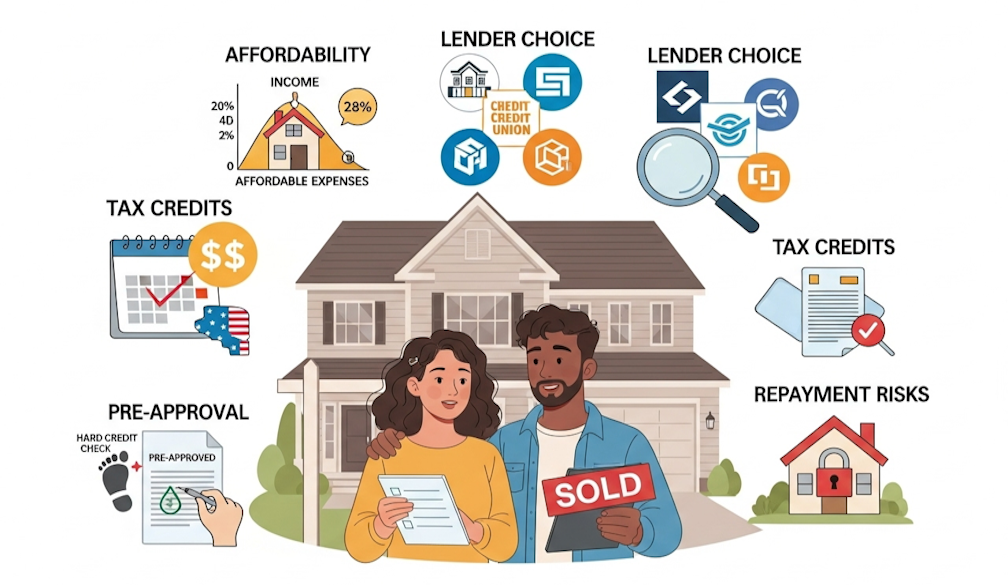

1. Be aware of how much you can afford as a first-time buyer

We all have big dreams of the type of home we want to live in but it’s also important to be realistic. Your first home may not be your last, and with finances and market conditions a key factor, you may not be able to get your dream home right away.

To avoid disappointment, put together a budget listing your full income and outgoings each month to get an idea of how much you can commit to a mortgage. Ideally, house payments shouldn’t account for more than 28% of your gross monthly income (known as the 28/36 rule). If you multiply your monthly income (before tax) by 0.28 this will tell you where your limit should be.

Also, don’t forget that you will have to include your deposit in this figure, as that will be the first lump sum payment you will have to make towards your new home.

2. Take your time choosing the right lender for your mortgage

On the upside, finding a mortgage lender is easier than it’s ever been, as there are so many options to choose from. However, the downside is that if you are a first-time buyer, it is possible to feel overwhelmed by all the numbers and offers being advertised.

Take your time to do your research and get quotes from 3-4 different lenders to compare the repayment terms, interest rate and other key variables. You’ll need to choose between a fixed-rate or variable rate mortgage, and a specialist lender may be a better option if you have an adverse credit history.

Whether you’re looking for a mortgage in Pennsylvania, Tennessee, Iowa or anywhere else in the country, weigh up the pros and cons of the lenders you are thinking of applying to ensure you find the best match for your needs.

3. Check your tax credit options

Although the First-Time Homebuyer Tax Credit introduced during the 2008 financial crisis is no longer available, there may be other options available to you (First-Time Homebuyer Tax Credit Act of 2025 is on the horizon, although it has not yet been passed into federal law).

If you purchased discounts points for your mortgage, these could help to reduce some of the interest costs, which tend to be heavier for brand-new mortgages. Depending on the state you live in, you may be able to claim a tax credit for some of the interest paid on your mortgage. Speak with your realtor and local government to see if there is any financial aid you can claim.

4. Getting “mortgage pre-approval” doesn’t guarantee you will be offered a full mortgage

Once you have found a suitable lender, the next thing to do is to get a mortgage pre-approval. Securing this from the bank can give you an advantage in a competitive housing market, potentially pushing you ahead of other buyers who are not able to demonstrate their financial suitability for a mortgage.

However, bear in mind that a mortgage pre-approval does not mean you are guaranteed a mortgage by the lender. The pre-approval only indicates what they may be willing to let you borrow, and they still need to underwrite the loan and ensure that the property meets their requirements.

When you make a formal application for a mortgage, you will undergo a fresh credit check. This means that the same information you provided for the pre-approval will be re-evaluated with the main difference being that the application will undergo a ‘hard’ credit check. The process involves a more detailed review of your finances, and it will leave a footprint on your credit report.

5. You could lose your home if you do not keep up repayments

Taking on a mortgage will be the most expensive financial commitment many people will make in their entire lifetime. It’s an exciting moment that should be enjoyed – although it’s also important to be aware of the risks involved.

The property you buy will be used as security against the mortgage. If you are unable to maintain the mortgage payments, there is a chance that you could have your home repossessed by the lender. This is often the last option, as most lenders usually try to find another solution, but it shouldn’t be ruled out entirely.

This goes back to our first point above – be careful with your finances and only take on a mortgage that you know you can afford. Not only can missing mortgage payments increase the risk of repossession, but it can damage your credit rating and make it more difficult to apply for finance in the future.

Final thoughts

Of course, there are more than 5 things first-time buyers will need to know about mortgages, but our list should give you some crucial fundamentals to consider. Create a detailed budget, do your research when it comes to lenders and see if there are any tax breaks you can use along the way. Don’t rely on your pre-approval as a guarantee that you will be offered a mortgage and only commit to a mortgage that you can afford, as defaulting can have serious consequences.