The budget super giveaway that allows the already wealthy to amass even more tax-free

- Written by: Peter Martin, Visiting Fellow, Crawford School of Public Policy, Australian National University

One of the strangest, certainly one of the hardest to justify, measures in last week’s budget was called “supporting retirees[1]”.

A better title would have been “supercharging the wealth of those retirees who already have more than enough to live on”.

It flies in the face of the findings of the government’s own retirement income[2] review and legislation it introduced partly in response earlier this year[3].

It happens not to support the living standards of retirees at all. It will enable some to spend less on themselves than they would have, while enabling those with serious wealth to accelerate the accumulation of even more, tax-free.

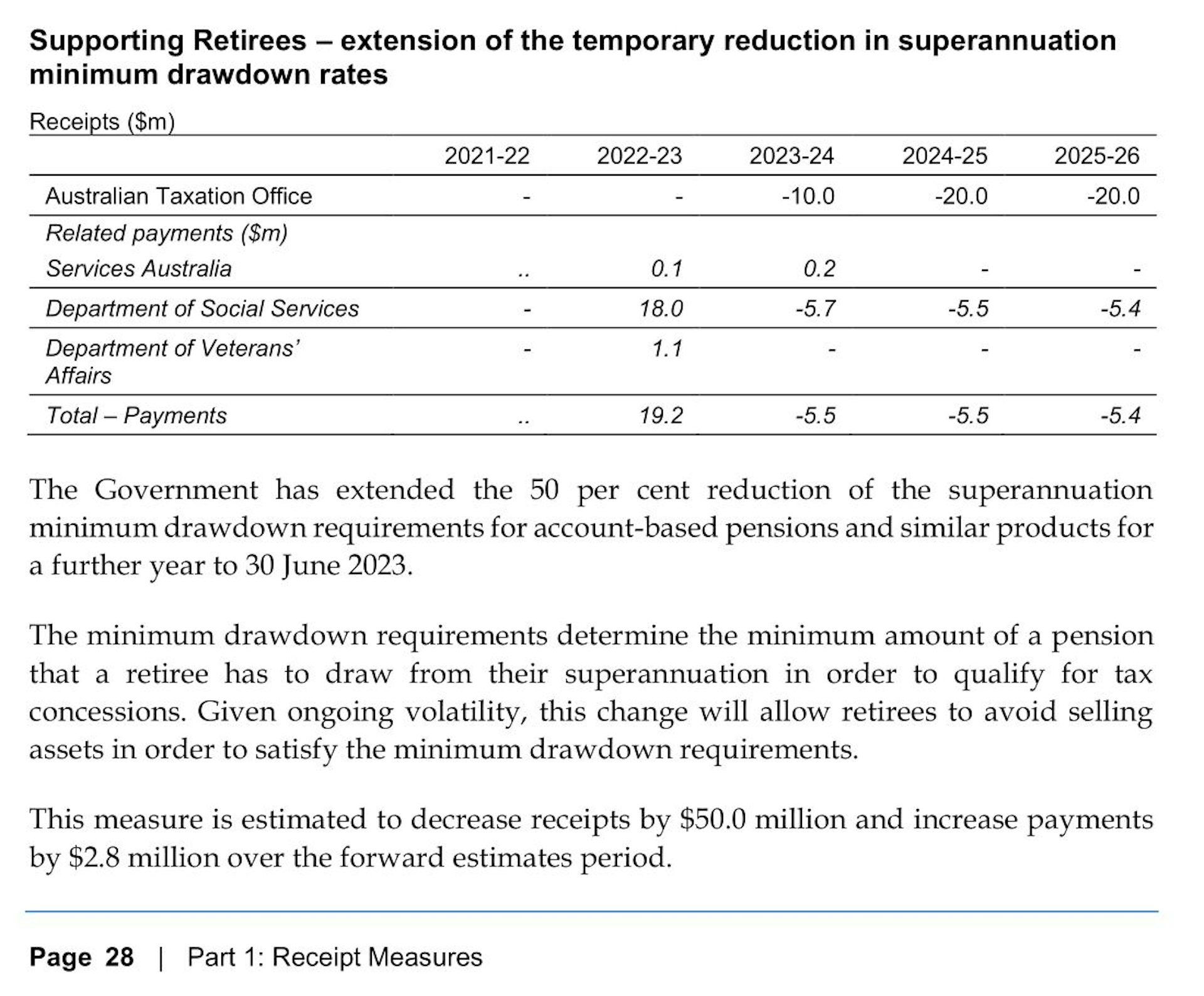

What the measure does is extend a temporary[4] COVID relaxation of the rules requiring retirees to actually withdraw a minimum amount from their super each year, introduced in March 2020 when financial markets were in free-fall.

All retirees are required to withdraw a minimum amount from super each year in order to ensure it isn’t simply used as a vehicle to accumulate tax-free savings that aren’t used.

Retirees have to withdraw a minimum per year

For retirees aged 65-74 the regulated minimum is 5%[5] per year, for those aged 75-79 it is 6% per year and so on, up to retirees aged 95 and over, who are required to withdraw at least 14% per year.

Nothing stops retirees withdrawing more than the regulated minimum, but the review found that in practice the typical withdrawal rate is just above the minimum, because people use it as an “anchor” or guide to what to do.

It identifies the most common misconception[6] about super being that

“the minimum drawdown rate is what the government recommends”

It says another is: “I should only draw down the income earned on my assets, not the capital”. Both set up retirees for a much lower standard of living than they could get.

The review finds that if a middle earner drew down an optimum amount rather than the minimum required, his or her super income would be 20% higher[7].

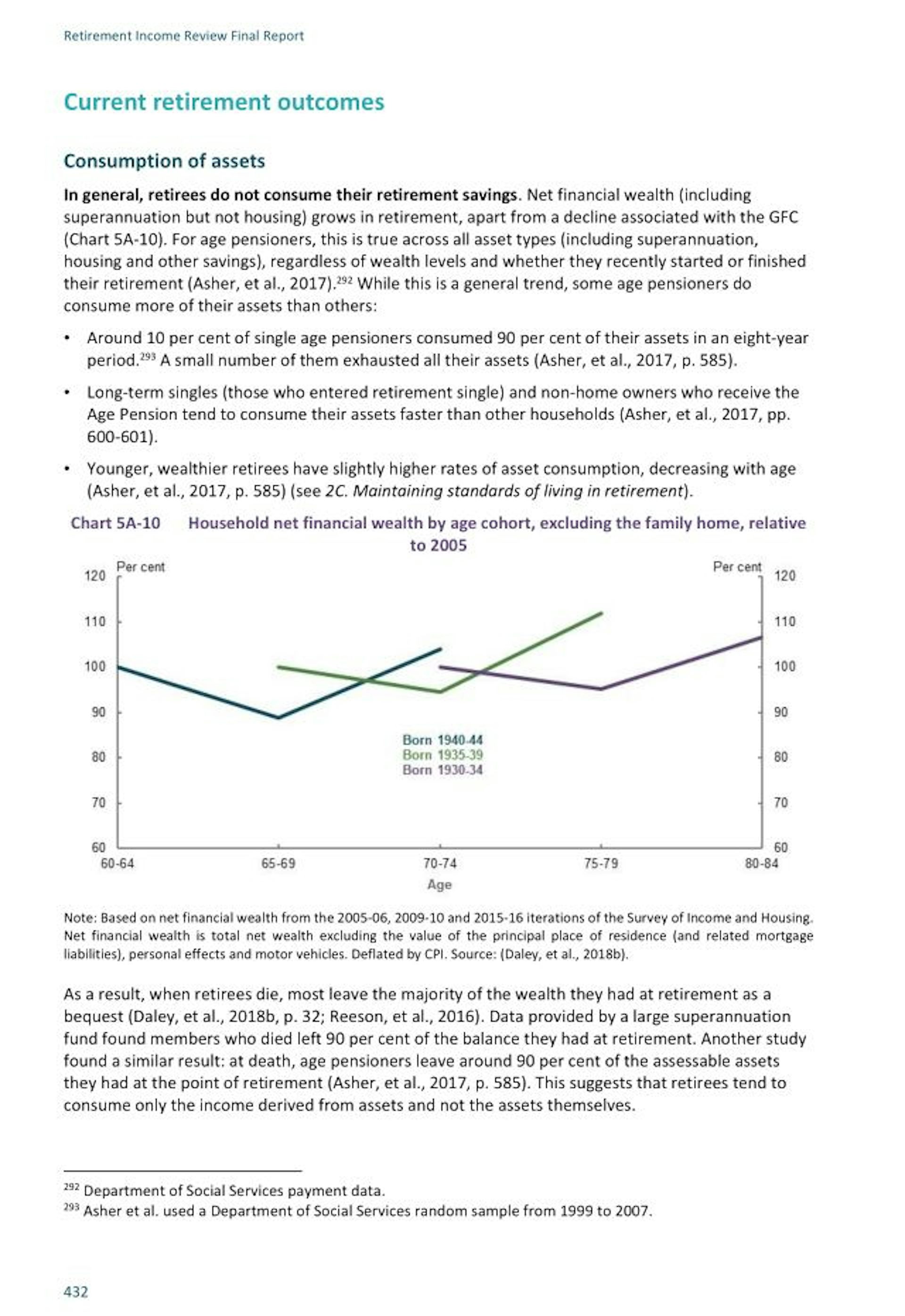

Instead, most retirees “die with the bulk of their wealth intact”. One fund told the review its members who died left 90% of the balance they had at retirement[8].

Most die with most intact

It’s at odds with the purpose of super, defined by the government as to provide “income in retirement[9]”. In February the government legislated to help make sure this is what funds did. From July they will be required to present to their members with an income strategy[10], for which bequests “should not be an aim[11]”.

Things changed when the Australian share market collapsed 30% between mid-February and mid-March 2020 as coronavirus took hold.

As a “temporary[12]” measure, Treasurer Josh Frydenberg halved[13] the drawdown requirements, in order to enable retirees to better build up their balances after the storm passed. A similar measure was introduced during the global financial crisis.

The storm passed quickly. Markets began climbing back the day the treasurer made the announcement, and then kept climbing. SuperRatings says in the past year the median balanced super fund has grown 13.4%[14].

Yet oddly, the government extended the measure in May last year[15] when the market was soaring to new heights, in order to “make life easier for our retirees” and then extended it again on budget night[16] in order to “recognise the valuable contribution self-funded retirees make to the Australian economy”.

It is as if the government has junked the idea that super should actually be used to provide income to the people who accumulate it.

As it happens there is nothing in the drawdown requirements that forces retirees to spend on themselves (and nor could there be). All they do is force retirees to withdraw a minimum amount from the generally tax-free environment that is retiree super, and have it treated like other people’s investments and savings.

Earnings in retiree super untaxed

If retirees aren’t forced to withdraw a minimum, in the words of the retirement income report to the treasurer, large amounts will be held in super “mainly as a tax minimisation strategy[17], separate to any retirement income goals”.

The only justification offered in budget papers (a weak one) refers to “ongoing volatility” and the need to “allow retirees to avoid selling assets[18]”.

But markets are generally volatile, and it is usually super funds that sell assets, not retirees. It’s as if the measure is directed at self-managed super funds, some of which are rich beyond most of our wildest dreams, certainly far too rich to need to pay out anything but a tiny percentage of their holdings to their members.

Read more: No longer temporary, the super changes will most help tax dodgers[19]

A freedom of information request by the Australian Financial Review has revealed that 27 such funds hold more than A$100 million[20] each. Its best guess is they are owned by Australia’s wealthiest families.

Of course, most retirees have much lower balances, and are reluctant to withdraw funds for another reason[21]. Perhaps surprisingly, studies examined by the review find that main reason isn’t a desire to pass on an inheritance to their children.

Overwhelmingly, retirees are concerned about “outliving their savings[22]”.

Frightened of outliving savings

The prospect of inferior aged care or a late health emergency compels most retirees to save far more than they are likely to need, just in case.

Many are unaware of how little end-of-life aged and health care can cost (“especially given the complexity of aged care means-testing arrangements”) and many more want to buy their way out of standard care because of the awful things they have heard, some of it in the aged care royal commission[23].

Read more: Labor's budget reply goes big on aged care, similar on much else[24]

It makes Labor’s budget reply promise of more money for aged care[25] and a nurse on each site 24/7 doubly attractive. It might stop us hanging on to absurd amounts of our super out of fear.

It might allow us to relax and enjoy what could be the best decades of our lives.

References

- ^ supporting retirees (images.theconversation.com)

- ^ retirement income (treasury.gov.au)

- ^ earlier this year (ministers.treasury.gov.au)

- ^ temporary (ministers.treasury.gov.au)

- ^ 5% (classic.austlii.edu.au)

- ^ the most common misconception (treasury.gov.au)

- ^ 20% higher (images.theconversation.com)

- ^ 90% of the balance they had at retirement (images.theconversation.com)

- ^ income in retirement (www.legislation.gov.au)

- ^ income strategy (ministers.treasury.gov.au)

- ^ should not be an aim (treasury.gov.au)

- ^ temporary (ministers.treasury.gov.au)

- ^ halved (ministers.treasury.gov.au)

- ^ 13.4% (www.lonsec.com.au)

- ^ May last year (ministers.treasury.gov.au)

- ^ budget night (cdn.theconversation.com)

- ^ mainly as a tax minimisation strategy (treasury.gov.au)

- ^ allow retirees to avoid selling assets (images.theconversation.com)

- ^ No longer temporary, the super changes will most help tax dodgers (theconversation.com)

- ^ A$100 million (www.afr.com)

- ^ another reason (grattan.edu.au)

- ^ outliving their savings (treasury.gov.au)

- ^ aged care royal commission (theconversation.com)

- ^ Labor's budget reply goes big on aged care, similar on much else (theconversation.com)

- ^ more money for aged care (theconversation.com)

Authors: Peter Martin, Visiting Fellow, Crawford School of Public Policy, Australian National University

{kind=link}

{kind=link}

{kind=link}